To deepen our understanding of this transition, Zavala Civitas has launched a Middle East Governance & Succession Committee led by Senior Advisor Carla Geday. The committee brings together regional expertise, applied research and on-the-ground insights from family enterprises across the GCC.

Its mandate is clear: to study emerging governance challenges, succession trends, and the leadership capabilities Middle Eastern family businesses will require in the next decade. The analysis below forms part of that ongoing research effort.

Family-owned enterprises don’t just shape the Middle Eastern economy. They are its foundation. According to New York University Abu Dhabi’s Family Business Histories project, more than 80% of companies across MENA are family-run. In the GCC, their weight is even greater: family firms represent over 60% of private-sector wealth, according to Quwa Legal. In the UAE alone, the Ministry of Economy reports that family businesses contribute around 60% of GDP, employ more than 80% of the workforce and make up nearly 90% of private-sector companies.

With such influence, the region’s economic resilience depends heavily on the continuity of these enterprises. This continuity now hinges on one crucial factor: succession planning. Nearly US$1 trillion in family wealth is expected to transition across generations in the GCC by 2030, according to McKinsey analysis cited by Gulf Business and DIFC. The question is not whether families should prepare for leadership change. The question is whether they can afford not to.

The shift from tradition to structured succession

For decades, succession in family businesses across the Gulf relied on trust, seniority and unspoken rules. Roles were understood rather than documented, and key decisions stayed within the family. In a less regulated and more relationship-driven environment, this worked well.

Today the context is different. Cross-border operations, institutional investors and higher regulatory expectations have increased the complexity and risk surrounding leadership transitions. Trust still matters deeply, but trust without structure becomes fragile at the moment of succession.

A 2025 study by Lombard Odier highlights this structural gap. Only 18% of GCC family businesses have a comprehensive succession plan, yet 96% of senior leaders and 93% of next-generation members express confidence in their ability to take the company forward. Confidence is high, but readiness is not. The same study shows that many families recognise the importance of succession but leave planning for later, often too late.

At the same time, expectations from younger leaders are changing. According to Lombard Odier, 79% of next-generation respondents intend to work with advisers who align better with their values and digital expectations. They prioritise transparency, innovation, internationalisation and the inclusion of women in leadership roles. These expectations make structured succession planning not only important but urgent.

How governance and succession planning reinforce each other

Governance reforms are advancing across the region, but their greatest impact is felt when they enable predictable, stable and fair leadership transitions. Research by the Pearl Initiative and PwC shows that succession, conflict resolution and role clarity remain the top governance challenges for GCC family firms. Tensions often arise not from strategy or performance but from uncertainty over who will lead, under what conditions and at what moment.

Legal frameworks across the GCC are evolving to address these issues. According to Quwa Legal, families are increasingly formalising their structures through shareholder agreements, constitutions, trusts and holding companies. Recent reforms in the UAE and Saudi Arabia strengthen governance codes and introduce new vehicles, such as private foundations, to support long-term succession structures.

Investor behaviour also plays a role. PwC’s Private Equity and Family Business Survey shows that around 90% of businesses globally are now open to private equity, up from just 18% in 2011. Investors look for governance structures that ensure decisions will remain consistent and transitions will not disrupt value creation. Succession planning becomes the anchor that gives governance its real operational meaning.

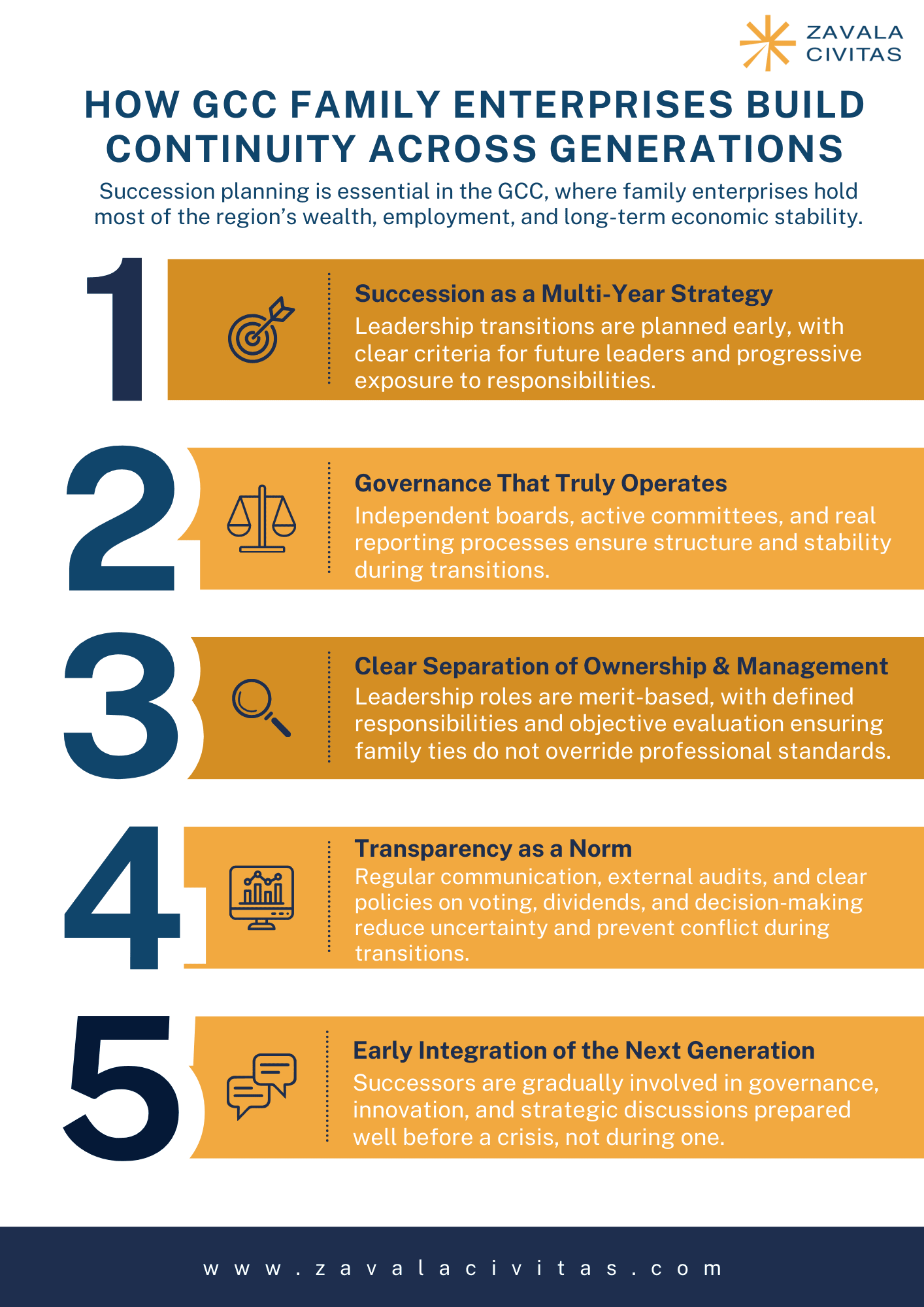

What distinguishes succession-ready family enterprises

The most resilient family-owned businesses in the region are not necessarily the largest or the oldest. They are the ones that approach succession with discipline and intention. Their practices often include:

- Succession as a multi-year strategy.

Leadership transitions are planned early. Families define clear criteria for leadership roles and prepare successors through structured exposure and responsibility. - Governance that operates, not decorates.

Boards with independent directors, functioning committees and real reporting mechanisms create the structure needed for smooth transitions. - Clarity between ownership and management.

Members in leadership roles are selected and evaluated on merit. Responsibilities are defined and performance is assessed objectively. - Transparency as a standard.

Regular communication, external audits and clear policies around voting, dividends and decision-making reduce uncertainty during transitions. - Integration of the next generation.

Successors are not kept on the side-lines until a crisis emerges. They are gradually involved in strategic discussions, innovation initiatives and governance bodies.

A Middle East priority with economic implications

Because family enterprises represent such a large share of private-sector wealth and employment, it becomes a regional economic priority. Unplanned or contested transitions can affect access to credit, investor confidence, business continuity and job stability.

The data is consistent. Family businesses in the Middle East remain confident, ambitious and central to the region’s economic future. But a minority have established frameworks that can support generational transition. With nearly US$1 trillion set to change hands in the coming years, the cost of avoiding structured succession planning has grown exponentially.

Family-owned enterprises have fuelled the economic development of the GCC for generations. Their next challenge is continuity. Structured succession planning is the most important tool they have to protect leadership, capital and legacy.

This is not a matter of replacing a founder. It is a multi-year, strategic process that ensures decisions can outlast personalities and preserve unity. Designed well, succession planning strengthens governance, builds trust inside and outside the family, and positions the business for long-term resilience.

Legacy is inherited. Continuity is built. Succession planning is how the region’s family enterprises can secure both.

Click here to get in contact with our middle east committee.